Net Revenue Retention: The SaaS Metric That Predicts Growth

Net Revenue Retention might be the most important metric for SaaS companies that investors and operators rarely discuss publicly. It tells you whether your existing customers are worth more or less over time. A company with 120% NRR can grow significantly even without acquiring a single new customer. A company with 80% NRR is fighting against a constant drain that no amount of acquisition spending can fix.

I’ve analyzed SaaS metrics for years, both for my own products and for clients building subscription businesses. NRR consistently separates great businesses from mediocre ones. I’ve seen two companies with identical MRR where one was thriving and the other was slowly dying… the difference was always NRR. Companies with strong NRR attract higher valuations, have more predictable revenue, and can invest more aggressively in growth. Understanding this metric transforms how you think about customer success and product development.

What Is Net Revenue Retention?

Net Revenue Retention (NRR) measures the revenue from your existing customer base over time, accounting for expansions, contractions, and churn. It answers a simple question: If you stopped acquiring new customers today, would your revenue grow or shrink?

That’s it. One metric that tells you whether you’re building on solid ground or on sand.

The formula is central to SaaS marketing and growth planning:

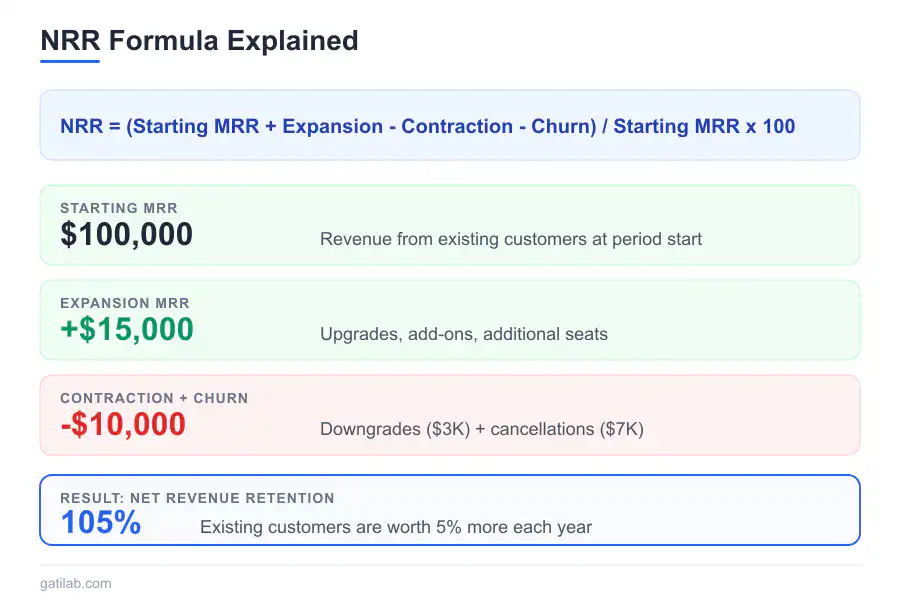

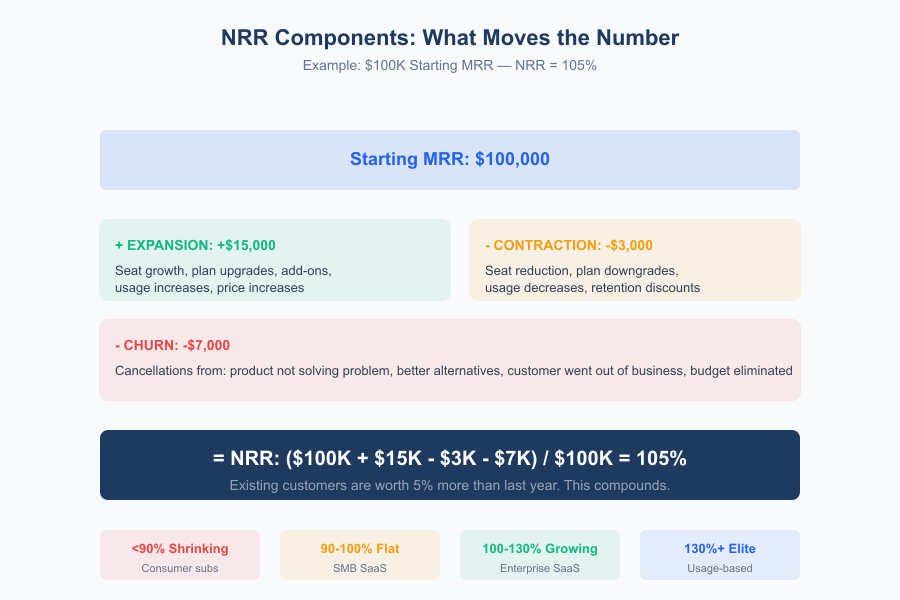

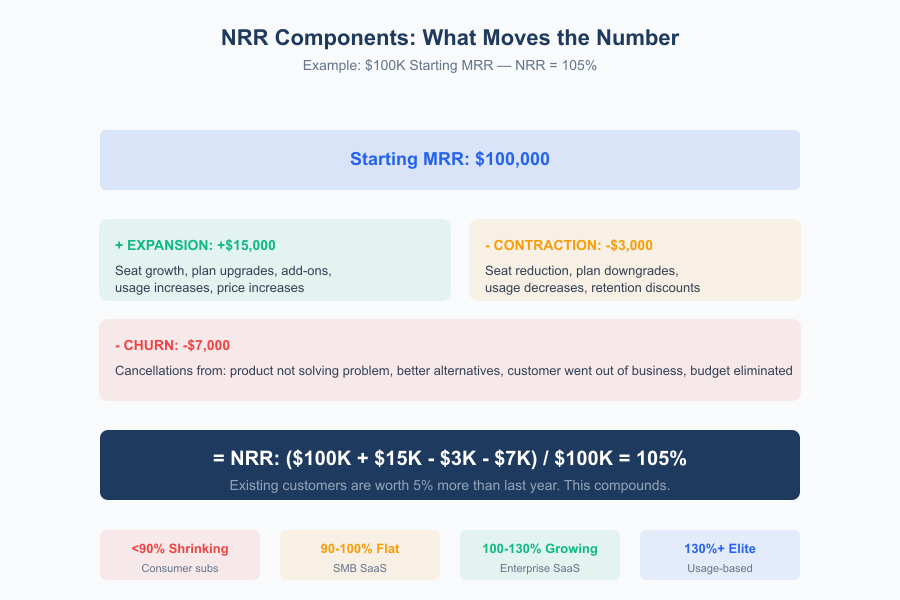

NRR = (Starting MRR + Expansion – Contraction – Churn) / Starting MRR x 100

Let me break down each component.

Starting MRR is your monthly recurring revenue from existing customers at the beginning of the period. This is your baseline.

Expansion MRR is additional revenue from those same existing customers. Upgrades, add-ons, additional seats, or increased usage. This is the good stuff.

Contraction MRR is lost revenue from downgrades. Customers still paying, but less than before. They haven’t left, but they’ve pulled back.

Churned MRR is revenue lost from customers who cancelled entirely. Gone.

Here’s a concrete example. If you started with $100,000 MRR, gained $15,000 from expansions, lost $3,000 from downgrades, and lost $7,000 from cancellations, your NRR is:

($100,000 + $15,000 – $3,000 – $7,000) / $100,000 x 100 = 105%

Your existing customers are worth 5% more than they were a year ago. That 5% compounds. Over five years, it transforms your revenue trajectory completely.

Why NRR Matters

It reveals product-market fit. High NRR means customers find increasing value in your product. They’re not just staying. They’re paying more. This is the strongest signal that your product solves real problems, and I’d argue it’s a better signal than acquisition metrics because it measures what happens after the sale.

It determines growth efficiency. With NRR over 100%, every dollar spent on acquisition gets multiplied over time. With NRR under 100%, you’re constantly backfilling lost revenue before you can grow. I’ve watched companies spend aggressively on acquisition while their existing customer base quietly eroded. It’s like filling a bathtub with the drain open.

It attracts investors. SaaS companies are valued on multiples of revenue. High NRR companies command higher multiples because their revenue is more durable and growing. The difference between 80% and 120% NRR can mean billions in valuation difference for large companies. Even for smaller businesses, NRR directly impacts what acquirers will pay.

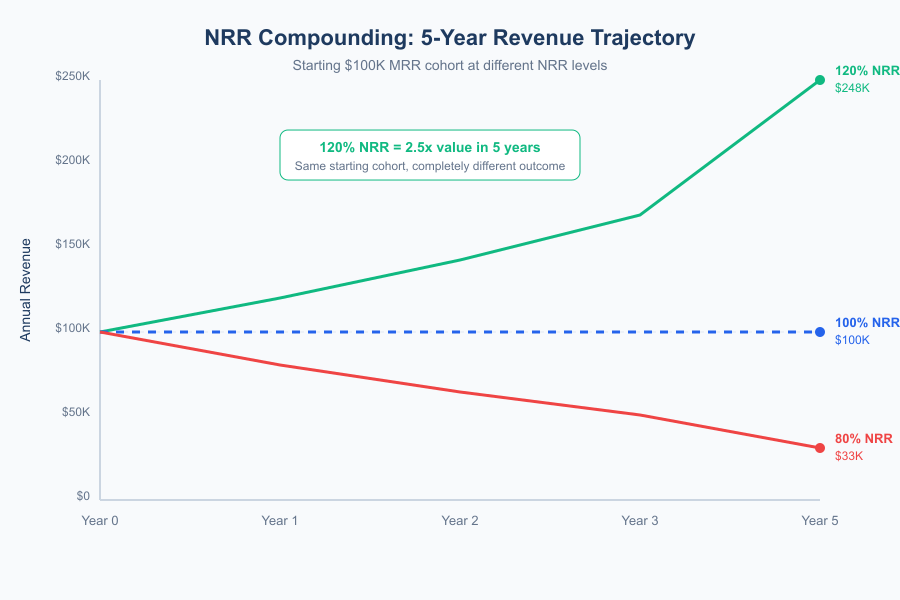

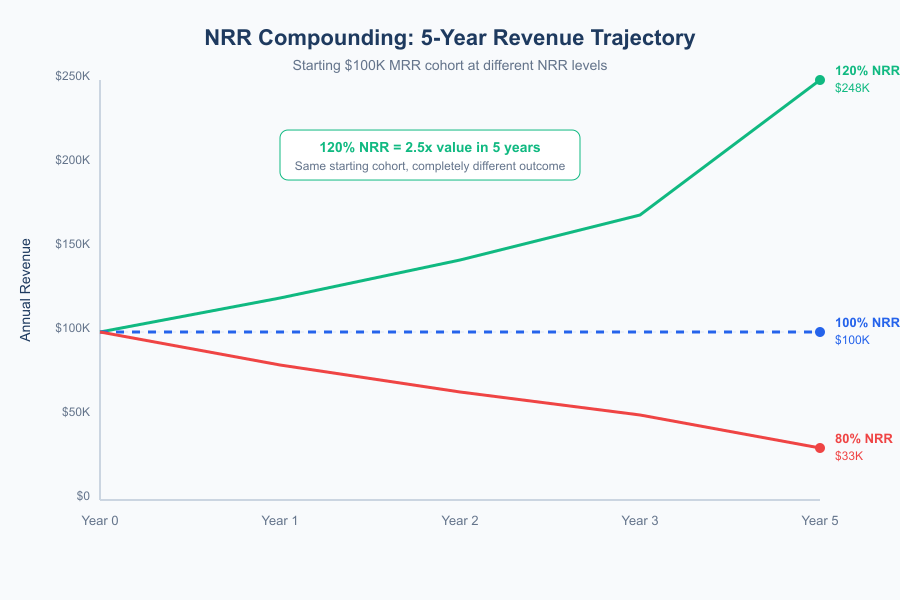

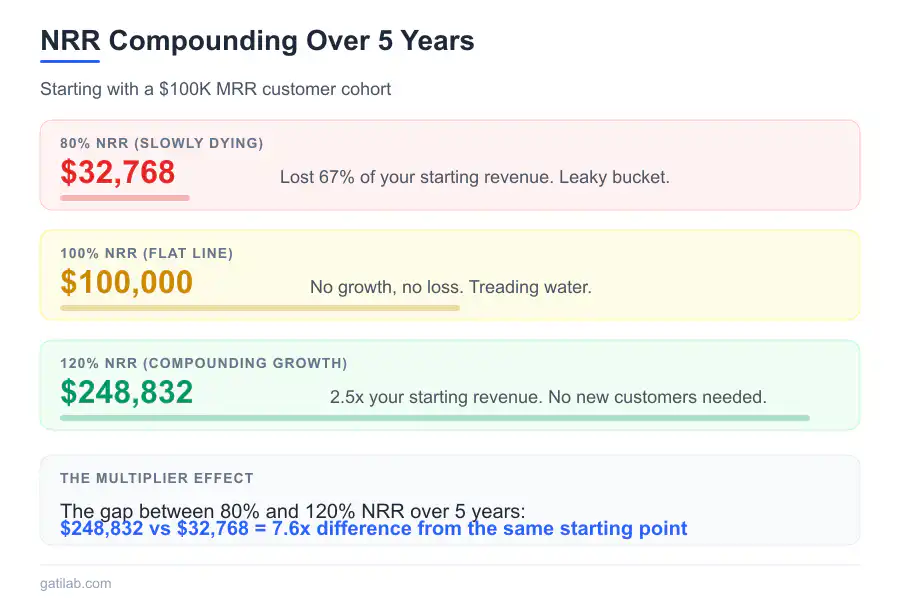

It compounds dramatically. Small differences in NRR compound over years. A cohort of customers at 120% NRR is worth 2.5x as much after 5 years as the same cohort at 100% NRR. That’s not a marginal difference. That’s a completely different business.

NRR vs Other Retention Metrics

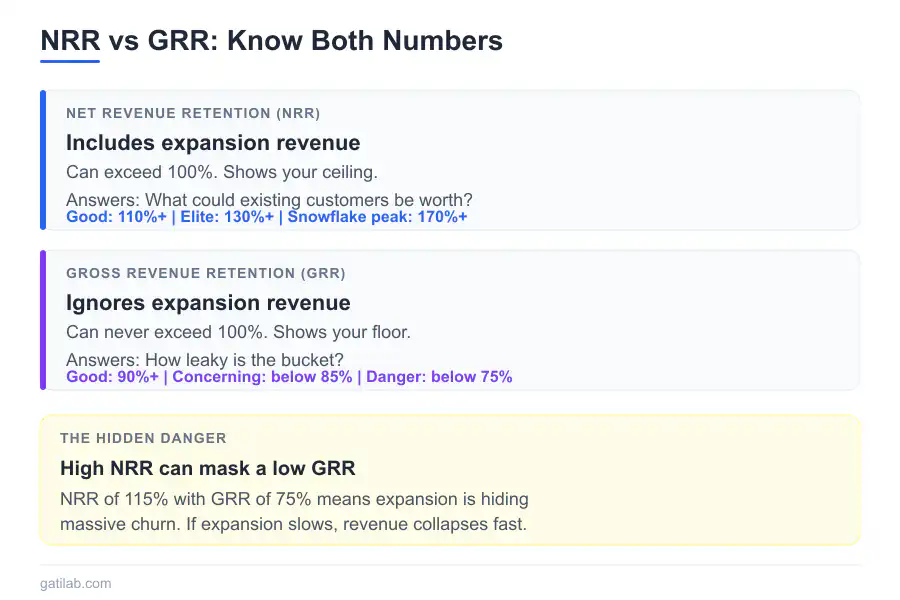

Gross Revenue Retention (GRR) ignores expansion. It only measures how much of your starting revenue you kept:

GRR = (Starting MRR – Contraction – Churn) / Starting MRR x 100

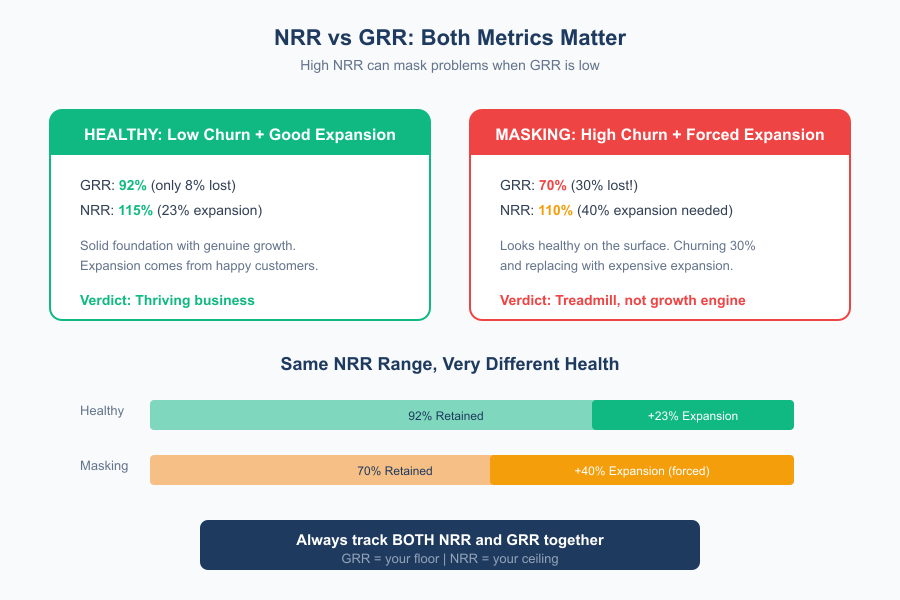

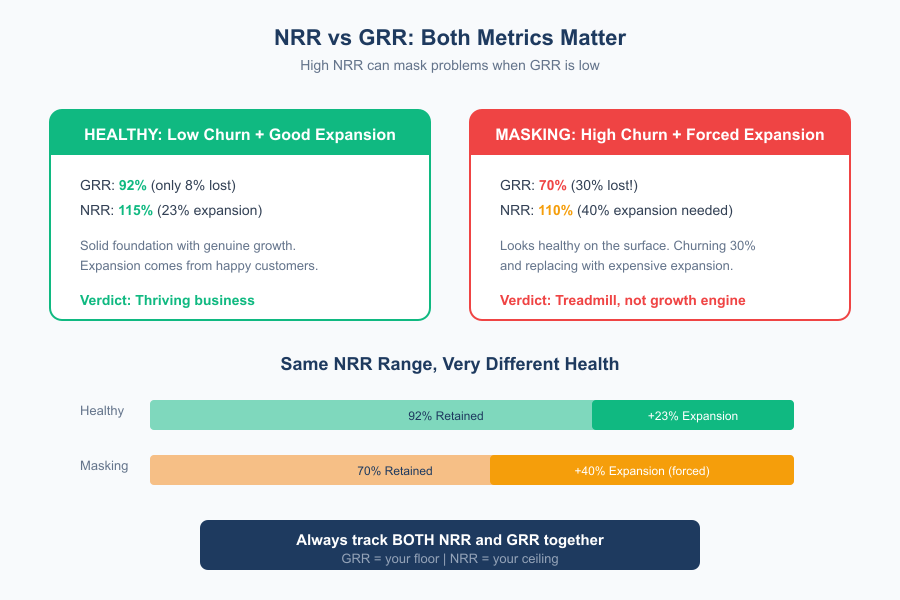

GRR can never exceed 100%. It measures your floor, how much you’re keeping. NRR measures your ceiling, what existing customers could be worth. I always look at both. GRR tells me if I have a leaky bucket. NRR tells me if expansion is masking those leaks.

Logo Retention (Customer Retention) counts customers, not revenue:

Logo Retention = (Starting Customers – Churned Customers) / Starting Customers x 100

A company could have 90% logo retention but 80% revenue retention if larger customers churn more. Or 80% logo retention but 110% NRR if remaining customers expand significantly. I’ve seen both scenarios, and the second one is surprisingly healthy despite looking bad on the surface.

Dollar Retention is often used interchangeably with NRR. Some companies calculate it slightly differently, but the concept is the same.

NRR Benchmarks

NRR varies dramatically by segment, and knowing where you should be prevents both complacency and panic.

Enterprise SaaS with large contracts typically sees 110-130%+ NRR. Enterprise customers expand as they adopt more features, add departments, and integrate deeper. Snowflake reported over 170% NRR at its peak, which is extraordinary but reflects the usage-based model working perfectly.

SMB SaaS with smaller contracts typically falls in the 90-110% range. Smaller customers have less expansion potential and churn at higher rates. Below 90% is concerning and usually signals a product problem, a pricing problem, or both.

Consumer subscriptions normally see 80-95%. Individual users don’t usually expand. The focus is almost entirely on minimizing churn.

Usage-based products often see very high NRR (120%+) because successful customers naturally consume more over time. This is the model I find most interesting for new SaaS products.

The magic number is 100%. Above 100%, you grow from existing customers. Below 100%, you shrink without new acquisitions. It’s that simple.

The Components of NRR

Expansion revenue drives NRR above 100%. Sources include seat expansion when customers hire more people, plan upgrades when they move to higher tiers, add-on purchases for additional products, usage increases for usage-based pricing, and price increases that get passed through successfully.

The best expansion comes from genuine value delivery. Customers use your product more because it works. Forced upgrades through feature gating can work short-term but often creates resentment. I’ve seen companies gate features aggressively and then wonder why their NPS scores crater. The expansion revenue looked great for two quarters. The churn caught up by quarter four.

Contraction reduces NRR but keeps customers. It comes from seat reduction during layoffs or reorganization, plan downgrades from budget cuts or reduced needs, usage decreases during business slowdowns, and discounts offered to prevent churn.

Some contraction is inevitable. Economic downturns cause widespread seat reductions, and there’s nothing you can do about a customer’s budget getting cut. The goal is minimizing voluntary contractions where customers reduce usage because of dissatisfaction. That part is in your control.

Churn eliminates revenue entirely. Causes include the product not solving the problem, better alternatives existing, the customer going out of business, budgets being eliminated entirely, and poor customer experience.

Churn is the enemy. Even small churn rates compound into massive revenue loss over time. A 5% monthly churn rate means you lose over 46% of your customer base annually. The math is brutal.

Improving Expansion Revenue

Build expansion into your product. Design features that become more valuable at scale. Collaboration tools that improve with more users. Analytics that require more data storage. Workflows that span more departments. The expansion should feel natural, not forced.

The best expansion comes from genuine value delivery. Customers use your product more because it works. Forced upgrades through feature gating can work short-term but often creates resentment and accelerates churn by quarter four.

Price for growth. Per-seat pricing automatically expands with customer growth. Usage-based pricing expands with consumption. Flat-rate pricing caps expansion potential. I’ve moved away from flat-rate pricing on my own products specifically because it kills expansion revenue.

Launch complementary products. Give existing customers more to buy. Monday.com expanded from project management into CRM, marketing, and development tools. Each new product is an expansion opportunity. You don’t need to build everything at once, but having a roadmap for what existing customers might need next is essential.

Time upgrades to value delivery. Don’t push upgrades immediately. Wait until customers are successful with current features, then introduce premium capabilities. Success breeds expansion. Trying to upsell a customer who hasn’t found value yet just accelerates their path to churning.

Create expansion playbooks. Train customer success teams to identify expansion signals: customer hiring, new use cases mentioned, hitting usage limits. Proactive outreach at the right moment converts better than reactive sales. The signals are usually there if you’re paying attention.

Reducing Churn and Contraction

Fix onboarding. Most churn happens in the first 90 days. Customers who don’t reach value quickly cancel. Invest heavily in activation, guided setup, and quick wins. I’ve seen onboarding improvements cut churn by 30-40% without changing anything else about the product.

Monitor health scores. Build dashboards tracking engagement metrics like login frequency, feature usage, and support tickets. Declining health predicts future churn. Intervene early. Project management tools can help track these customer health indicators systematically.

Create switching costs. Integrations, data dependencies, and workflow embedding make leaving painful. Not in a predatory way, but by making your product deeply embedded in how customers work. When leaving means rebuilding processes from scratch, customers think twice about switching over a minor price difference.

Deliver ongoing value. Regular feature releases, educational content, and proactive support remind customers why they pay. Stagnant products invite churn. If your product looks the same as it did when they signed up 18 months ago, they’ll start wondering if it’s still worth paying for.

Save at-risk customers. Have a process for rescue. When customers signal intent to cancel, route them to retention specialists with authority to offer discounts, free months, or custom solutions. This isn’t about being desperate. It’s about understanding why they’re leaving and addressing it if you can.

Analyze churn patterns. Which customer segments churn most? At what point in the lifecycle? For what reasons? Pattern recognition reveals systemic issues that no amount of individual customer rescue can fix.

Calculating and Tracking NRR

Choose your time period. Monthly NRR fluctuates more but shows trends faster. Annual NRR is smoother and preferred for reporting. Quarterly balances both. I track monthly but report quarterly, and I look at the trailing 12-month number for strategic decisions.

Define your cohort. Track NRR for customers who started in a specific period. This shows how retention changes over time and isolates the effect of different acquisition channels or product versions. Cohort analysis has shown me things aggregate numbers completely hid.

Separate segments. Calculate NRR by customer size, industry, acquisition source, and product. Overall NRR hides important variations. Your enterprise segment might have 130% NRR while SMB has 85%. Knowing that changes your strategy completely.

Build dashboards. Track NRR monthly alongside its components. Seeing expansion, contraction, and churn separately reveals what’s driving changes. A flat NRR number could mean stable business or could mean high expansion offsetting high churn. Very different situations.

Compare to CAC payback. If NRR is 120% and CAC payback is 12 months, every customer becomes profitable and then keeps growing. If NRR is 80% and CAC payback is 18 months, you’re losing money on most customers before they churn. The combination of these two metrics tells you more about business health than either one alone.

NRR in Practice

Slack achieved high NRR through viral expansion. As teams adopted it, they added more users. As users loved it, they advocated for company-wide rollout. Organic expansion drove NRR well over 100%. The product basically sold itself into larger contracts without a sales team pushing it.

Zoom saw NRR explode during COVID as existing customers massively increased usage and seat counts. Usage-based elements combined with seat expansion created extraordinary retention metrics. An unusual situation, but it demonstrated what happens when a product becomes genuinely essential.

Salesforce maintains strong NRR through constant platform expansion and upselling. Customers start with Sales Cloud, then add Service Cloud, Marketing Cloud, and numerous add-ons. The platform strategy creates unlimited expansion headroom. They’ve essentially built an ecosystem where leaving means rebuilding your entire business workflow.

Snowflake achieved historically high NRR, sometimes exceeding 170%, through usage-based pricing. Successful customers analyze more data, which naturally increases consumption and revenue. The pricing model aligned perfectly with customer success.

Common NRR Mistakes

Celebrating high NRR while ignoring GRR. High NRR can mask high churn if expansion is strong. Check GRR too. If GRR is 70% but NRR is 110%, you’re churning 30% and replacing them with expensive expansion revenue. That’s not healthy. It’s a treadmill.

I’ve seen two companies with identical MRR where one was thriving and the other was slowly dying. The difference was always NRR. Companies with strong NRR attract higher valuations, have more predictable revenue, and can invest more aggressively in growth. It’s the metric that separates great SaaS businesses from mediocre ones.

Including new customer revenue in NRR. NRR only measures existing customers. If you include revenue from newly acquired customers, the metric becomes meaningless. I’ve seen pitch decks where “NRR” was actually total revenue retention including new logos. That’s not NRR. That’s something else entirely.

Not tracking cohorts. Overall NRR can hide declining cohort performance. If new cohorts have worse retention than old ones, you won’t see it in aggregate numbers until much later. By then, the problem is entrenched and expensive to fix.

Forcing expansion inappropriately. Aggressive upselling damages relationships and increases future churn. Sustainable expansion comes from value delivery, not sales pressure. I’ve seen sales teams celebrated for expansion revenue that was actually just pulling forward churn. The customer upgraded reluctantly, resented it, and left six months later.

Ignoring contraction. Some teams focus only on preventing cancellations while ignoring downgrades. Contraction erodes NRR just as effectively. It just takes longer to hurt. A customer downgrading from $500 to $200 per month is a $3,600 annual loss that nobody flagged because it wasn’t technically “churn.”

Building for High NRR

High NRR isn’t a goal you achieve through metrics optimization. It’s an outcome of building a product customers love, pricing it appropriately, and supporting customers effectively.

Start with product. Does your product solve increasingly important problems over time? Does it become more valuable as customers succeed? Does it expand naturally into adjacent use cases? If you’re answering no to all three, NRR optimization at the sales and success level won’t save you.

Align your pricing. Can customers pay more as they get more value? Per-seat and usage-based models create natural expansion. Feature-gated tiers encourage upgrades. The pricing structure either enables expansion or blocks it.

Invest in success. The customer success team drives expansion through relationship building, proactive outreach, and value demonstration. Underfunding success caps your NRR ceiling. Using the right CRM software can help track these relationships effectively and spot expansion opportunities before they pass.

Measure relentlessly. Track NRR by segment, cohort, and component. Understand exactly where retention comes from and where it fails. Data reveals opportunities that intuition misses. The companies I’ve seen build the strongest NRR are the ones that obsess over the components, not just the headline number.

SaaS Metrics FAQ

Frequently Asked Questions

What is Net Revenue Retention and how is it calculated?

Net Revenue Retention (NRR) measures revenue from existing customers over time, accounting for expansions, contractions, and churn. The formula is: NRR = (Starting MRR + Expansion – Contraction – Churn) / Starting MRR x 100. If you started with $100K MRR, gained $15K from expansions, lost $3K from downgrades, and $7K from cancellations, your NRR is 105%. Above 100% means you grow from existing customers alone.

What is a good NRR for SaaS companies?

Enterprise SaaS typically sees 110-130%+ NRR, with outliers like Snowflake hitting 170%+. SMB SaaS falls in the 90-110% range. Consumer subscriptions normally see 80-95%. The magic number is 100%. Above that, you grow from existing customers. Below that, you’re fighting a constant drain that no amount of acquisition spending can fix. Usage-based products often achieve the highest NRR at 120%+ because successful customers naturally consume more.

What is the difference between NRR and GRR?

Gross Revenue Retention (GRR) ignores expansion revenue and only measures how much of your starting revenue you kept. It can never exceed 100%. NRR includes expansion, so it can exceed 100% when existing customers pay more over time. GRR tells you if you have a leaky bucket. NRR tells you if expansion is masking those leaks. A company with 70% GRR but 110% NRR is churning 30% and replacing it with expensive expansion, which is not healthy.

How does NRR compound over multiple years?

Small NRR differences compound dramatically over time. A customer cohort at 120% NRR is worth 2.5x as much after 5 years compared to the same cohort at 100% NRR. At 80% NRR, you lose a third of that cohort’s revenue in just 2 years. The difference between 80% and 120% NRR can mean billions in valuation difference for large companies. Even for smaller businesses, NRR directly impacts acquisition efficiency and growth sustainability.

What drives expansion revenue in SaaS?

Expansion revenue comes from seat expansion (customer hires more people), plan upgrades (moving to higher tiers), add-on purchases (additional products), usage increases (usage-based pricing), and successful price increases. The best expansion comes from genuine value delivery where customers use your product more because it works. Forced upgrades through aggressive feature gating can work short-term but often creates resentment and accelerates churn by quarter four.

Why do investors care so much about NRR?

High NRR means revenue grows even without new customer acquisition. This signals strong product-market fit, efficient growth, and durable revenue. SaaS companies are valued on revenue multiples, and high NRR companies command significantly higher multiples because their revenue is more predictable and expanding. For acquirers and investors, NRR is the single best indicator of whether a business has a sustainable growth engine or is running on a treadmill.

How can I improve my company’s NRR?

Improve expansion through upsells, add-ons, and seat growth by building features that become more valuable at scale. Reduce churn by fixing onboarding (most churn happens in the first 90 days), monitoring customer health scores, and creating switching costs through deep integration. Minimize contraction by delivering ongoing value that justifies current spend. Per-seat and usage-based pricing models naturally create expansion opportunities that flat-rate pricing cannot.

Can NRR be too high and what are the warning signs?

Extremely high NRR (150%+) can indicate aggressive pricing on expansion or that you’re leaving money on the table with initial pricing. The main warning sign is high NRR paired with low GRR. If your NRR is 110% but GRR is only 70%, you’re churning 30% of customers and masking it with expansion from the remaining ones. That’s a treadmill, not a growth engine. Watch both metrics together to get the full picture.