Venture Capital for Service Businesses: Why It Rarely Works

Someone will tell you to raise money. Maybe an investor reaches out. Maybe a well-meaning advisor suggests it. Maybe you read about a funded competitor and feel behind.

Before you take that call, consider this: venture capital is designed for a specific type of business. Service businesses are not that type.

I’ve been building and running service businesses for over sixteen years. Not once have I needed or wanted VC money. Here’s why bootstrapping almost always beats funding for agencies, consultancies, and service-based companies.

The Venture Capital Model

Understanding VC requires understanding their math. And once you understand the math, you’ll see why your service business doesn’t fit the equation.

The portfolio approach:

A typical VC fund invests in 20-30 companies knowing most will fail. They need the winners to win big enough to cover all the losses and return the fund multiple times over.

This means every investment must have potential for 10x, 50x, or 100x returns. Modest success is failure in VC math. Let that sink in. Your profitable, growing, life-changing agency? In VC terms, it might be a write-off.

The timeline:

VC funds have fixed lifespans, typically 10 years. Investments made in year 2 need to exit by year 8-10. This creates pressure for rapid growth toward acquisition or IPO.

Slow and steady doesn’t work. Sustainable but modest doesn’t work. The model requires explosive growth on a fixed timeline.

The exit requirement:

VCs make money when they exit, selling their stake to another investor, acquirer, or public market. A profitable business that never exits returns nothing to the fund.

Your success isn’t their success unless there’s a liquidity event. Think about that. You could build a business that supports your family beautifully for decades, and your VC investor would consider it a failure.

Why Service Businesses Don’t Fit

Service businesses have structural characteristics that conflict with VC requirements. This isn’t a judgment on service businesses. It’s just math.

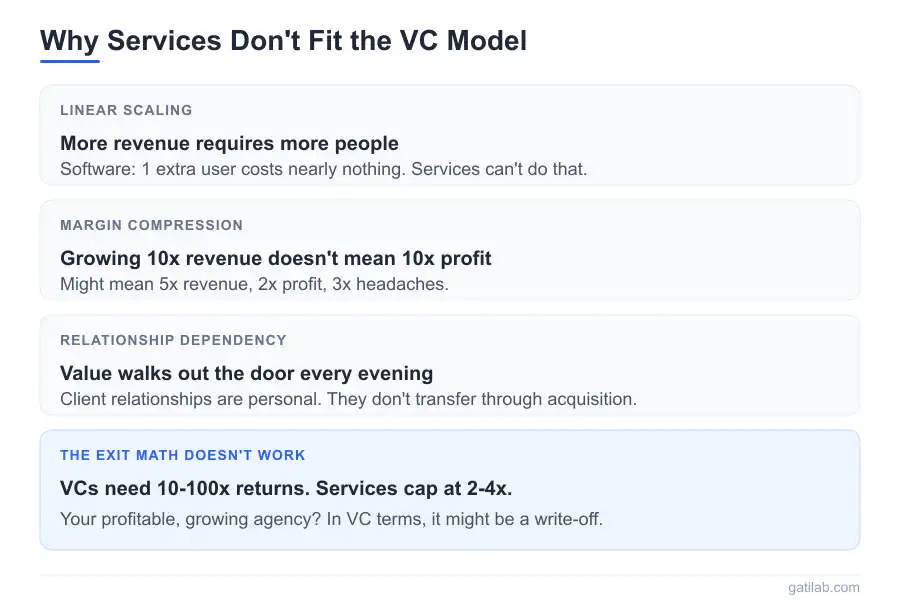

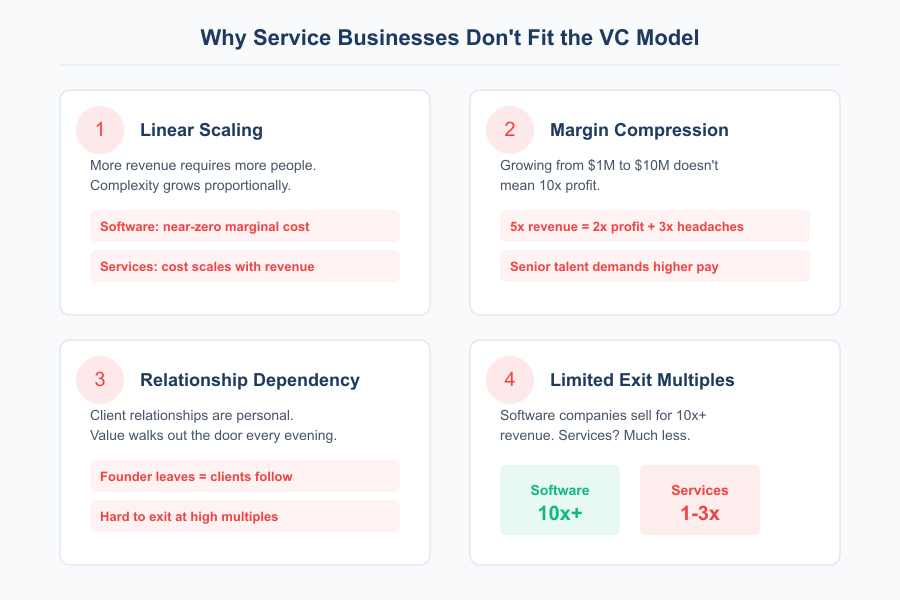

Linear scaling:

Services scale with people. More revenue requires more people. More people requires more management. Growth creates complexity proportionally.

This is fundamentally different from software where one more user costs nearly nothing to serve. The marginal economics don’t support venture scale. I’ve run the numbers on my own business multiple times. There’s no path to 100x that doesn’t break the model.

Margin compression:

As service businesses grow, margins often shrink. Senior talent demands higher salaries. Overhead increases. Utilization becomes harder to optimize.

Growing from $1M to $10M in revenue doesn’t mean 10x profit. It might mean 5x revenue and 2x profit with 3x headaches. I’ve watched this pattern play out with agencies in my network over and over.

Relationship dependency:

Client relationships are personal. They depend on specific people, specific trust, specific history. This doesn’t transfer easily through acquisition.

When the founder leaves, clients often follow. This makes service businesses harder to exit at high multiples. The value walks out the door every evening.

Limited exit multiples:

Software companies might sell for 10x revenue or more. Service businesses typically sell for 1-3x revenue, sometimes 3-5x for exceptional businesses.

Even a successful service business exit rarely generates VC-level returns. The math simply doesn’t work.

The Funding Trap

Taking VC money for a service business creates specific problems that I’ve watched play out in real time.

Growth pressure:

VCs expect rapid growth. In services, rapid growth means rapid hiring. Rapid hiring means quality dilution, culture erosion, and management overhead.

I’ve watched agencies double headcount in a year and spend the next two years recovering from the chaos. The pressure to grow fast conflicts directly with growing well. You can have one or the other, but rarely both.

Profitability punishment:

Profitable service businesses don’t need VC money. Taking it means either the business isn’t profitable or the money will be used to grow unsustainably.

VCs often push to sacrifice profitability for growth. In services, this creates cash flow crises that don’t occur in properly-bootstrapped businesses. I’ve seen it happen three times in the past five years to agencies I know personally.

Misaligned incentives:

The VC needs a big exit. You might want a sustainable, profitable business that supports your life for decades. These goals conflict fundamentally.

When conflicts arise, guess whose interests usually win? It’s not the founder who took the money.

Dilution reality:

Each funding round dilutes founder ownership. After Series A and B, founders often own 20-30% of their company. After a modest exit, that stake might be worth less than the salary they gave up building it.

The math works for billion-dollar exits. For service businesses, the exits are rarely that large. Run the numbers on your own scenario. You might be surprised how little you’d actually pocket.

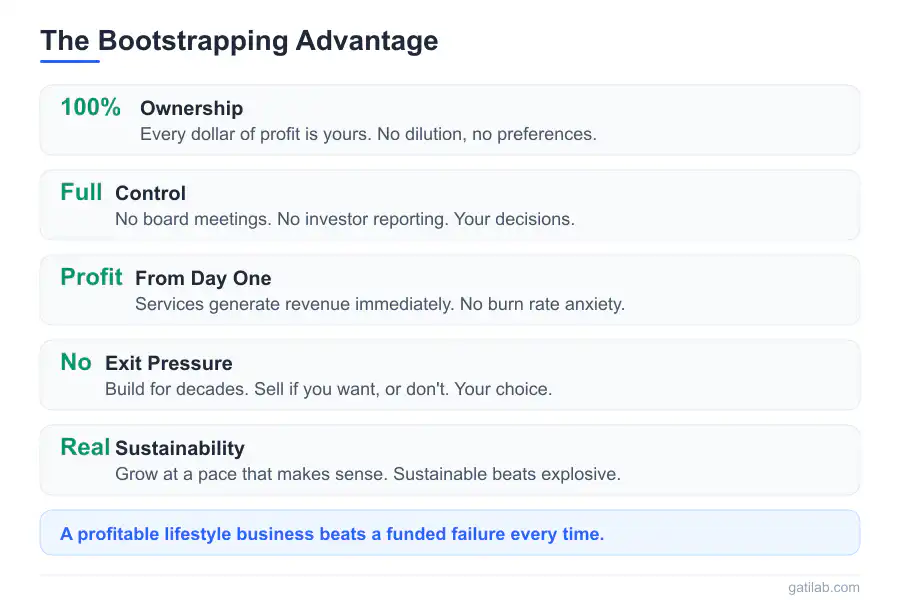

The Bootstrapping Advantage

Service businesses have natural advantages that bootstrapping preserves. These advantages are real, and they compound over time.

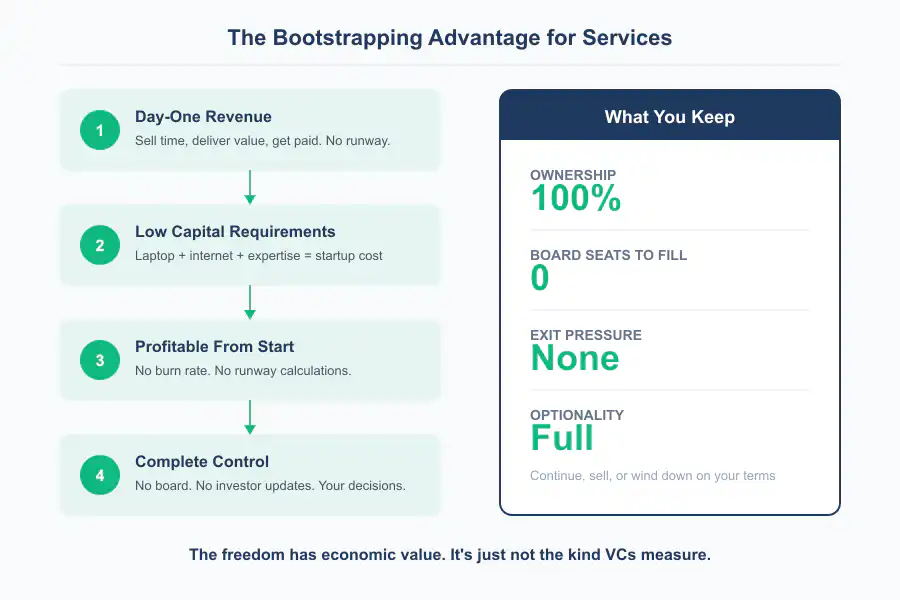

Day-one revenue:

Services generate revenue immediately. You sell time or expertise, deliver value, get paid. No product development runway. No years to product-market fit.

This makes external funding unnecessary for basic operations. You’re cash-flow positive from the start. My first month freelancing, I billed $3,200. Not life-changing, but it covered expenses. No VC check required.

Low capital requirements:

A laptop, internet connection, and expertise. That’s the startup cost for most service businesses. No servers to provision. No factories to build. No inventory to stock.

What would VC money even be used for? Hiring ahead of demand is dangerous. Marketing spend rarely works for high-touch services. The honest answer is often “I don’t actually need it.”

Profitable from the start:

Properly priced services are immediately profitable. Every project can generate margin from day one. This compounds into retained earnings that fund organic growth.

No burn rate. No runway calculations. No existential dependence on the next funding round.

Complete control:

Bootstrapped founders make decisions. Want to stay small? Your choice. Want to take a month off? No board to answer to. Want to pivot or wind down? Nobody’s stopping you.

Control isn’t just ego. It’s the ability to build the business that fits your life. After sixteen years, that freedom is worth more to me than any check.

What Bootstrapped Service Businesses Can Achieve

The limits are different than you might think.

Significant scale:

Bootstrapped agencies reach $10M, $50M, even $100M+ in revenue. Without external funding. With substantial founder ownership. With sustainable operations. Tracking growth with good accounting software helps maintain financial discipline along the way.

Scale is possible. Just not at venture velocity.

Real wealth creation:

A $5M agency generating 20% profit throws off $1M annually. Maintain that for a decade, and you’ve extracted $10M while building equity worth $5-15M.

No VC would fund this outcome. But it’s life-changing wealth for the founder. And you own 100% of it.

Optionality:

Bootstrapped businesses can choose their future. Continue indefinitely. Sell when the right offer comes. Wind down gracefully. The options remain open.

VC-funded businesses are on a one-way path. Grow and exit, or fail trying. There’s no in-between.

Sustainability:

Properly bootstrapped service businesses survive recessions, market shifts, and industry changes. They’re built for resilience, not explosive growth.

When growth stops (and it always eventually does), sustainable businesses adapt. VC-funded businesses implode. I watched this play out in 2020 and again in 2022. The bootstrapped businesses survived. Many funded ones didn’t.

When Funding Might Make Sense

I’m not categorically against funding. There are edge cases where it makes sense even for service-adjacent businesses.

Productizing services:

If you’re building software that automates your service delivery, you’re transitioning to a software company. Different rules apply.

But be honest: are you building a product, or are you justifying funding for a service business? I’ve seen founders convince themselves they’re “building a platform” when they’re really just running an agency that uses some internal tools.

Market consolidation:

If the strategy is acquiring competitors to build scale, capital accelerates that. Roll-ups can work in fragmented service markets.

But this is financial engineering, not organic business building. Different skills, different risks.

True platform plays:

If you’re building a marketplace or platform that matches service providers with clients, that’s a technology business wrapped in services.

The economics and scaling characteristics differ from traditional service businesses.

For most service businesses, these exceptions don’t apply. The default should be bootstrapping.

The Practical Path

How to build a service business without external capital. This is the path I’ve followed, and it works.

Start lean:

Begin as a solo consultant or small partnership. Keep overhead minimal. No office, no employees, no expenses that outpace revenue.

Revenue grows, then expenses grow. Never reverse this order. The moment you start spending money you haven’t earned, you’re introducing risk you don’t need.

Price for profit:

Your rates must include margin. Not “cover costs” but “generate profit.” Profit funds growth, emergencies, and eventually freedom. Our guide on pricing your services covers this in detail.

Underpricing services is the most common bootstrapping mistake. It works fine until you need capital you don’t have.

Hire slowly:

Each hire should be clearly funded by existing revenue. Not projected revenue. Not hoped-for revenue. Actual recurring revenue that supports the position.

Slow hiring builds better teams. People who join sustainable businesses stay longer. Every hire I’ve made based on “projected growth” ended up being premature.

Reinvest profits:

Growth capital comes from retained earnings. This is slower than VC funding but creates no obligations, no dilution, no external pressure.

The constraint is actually valuable. It forces discipline about which investments matter. When it’s your money, you think harder about where it goes.

Build recurring revenue:

Retainers, maintenance contracts, ongoing engagements. Recurring revenue provides stability and makes growth predictable. Our guide on building a retainer-based business model shows how to structure these relationships.

One-off projects create revenue volatility. Recurring relationships create sustainable businesses.

The Comparison

Let’s compare two scenarios. These are simplified but directionally accurate.

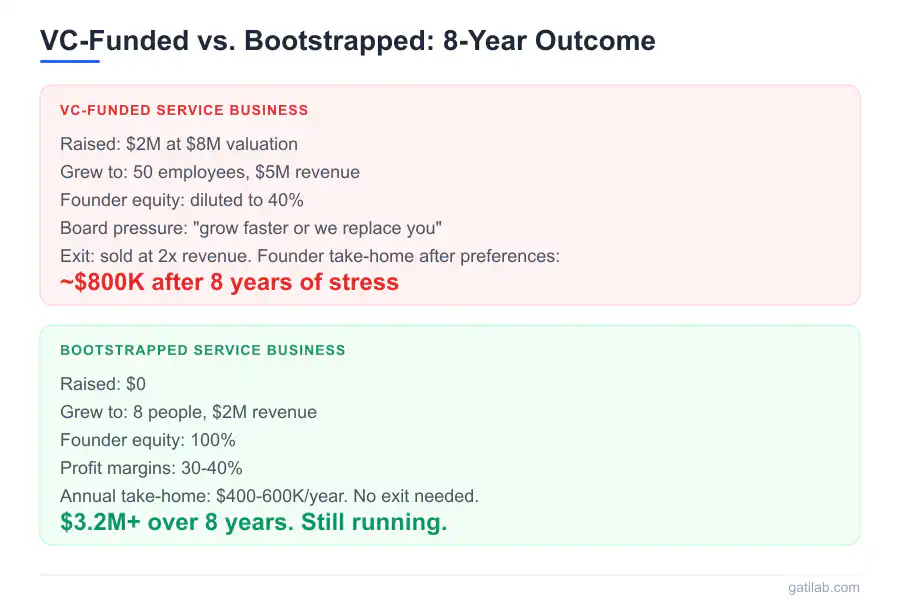

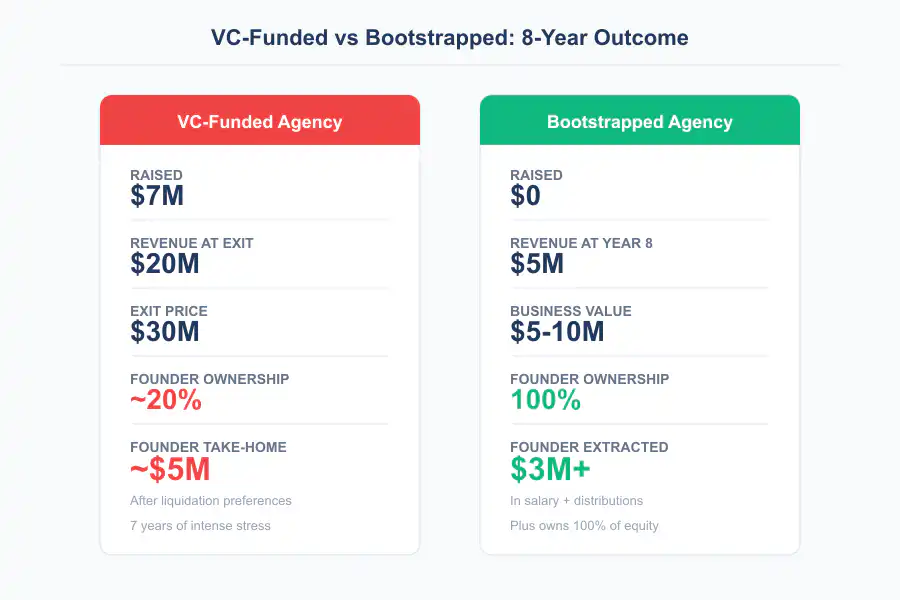

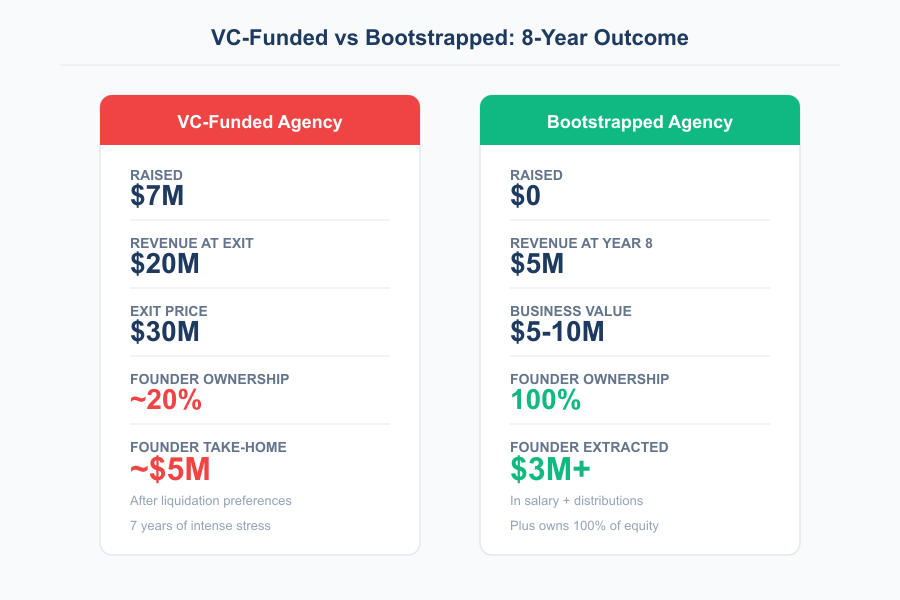

Scenario A: VC-funded agency

Raise $2M. Hire aggressively. Grow from $500K to $5M revenue in three years. Raise another $5M. Grow to $20M. Sell for $30M.

After liquidation preferences and dilution, founder walks away with maybe $5M after seven years of intense stress.

Scenario B: Bootstrapped agency

Start solo. Bill $200K year one. Hire first person year two. Grow organically to $2M revenue by year five. Continue to $5M by year eight.

Founder has extracted $3M+ in salary and distributions over eight years. Still owns 100% of a business worth $5-10M. Works 40-hour weeks. Takes vacations.

Which is actually better? The math isn’t obvious in VC’s favor. In fact, if you look closely, the bootstrapped founder often comes out ahead in both total wealth and quality of life.

The Pressure to Raise

Why do service business founders consider funding? Usually for the wrong reasons.

Competitive anxiety:

Funded competitors seem scary. They’re hiring aggressively, spending on marketing, undercutting on price.

But funded competitors often implode. Aggressive hiring creates management chaos. Marketing spend doesn’t work for trust-based services. Undercutting on price destroys margins. Watch funded competitors long enough and you’ll see many fail. I’ve outlasted several.

Growth impatience:

Organic growth feels slow. You want the business bigger now.

But why? What specifically improves at 2x size? Often the answer is “prestige” or “competition” rather than anything concrete. Be honest with yourself about what you’re actually chasing.

Validation seeking:

VC interest feels like validation. Someone smart thinks your business is worth investing in.

But VCs are often wrong. They’re pattern-matching, not evaluating your specific situation. Their interest isn’t wisdom. It’s a bet, and most of their bets lose.

The Freedom Factor

The deepest argument for bootstrapping is freedom. And I don’t mean that in a hand-wavy inspirational way. I mean it practically.

Your time:

Bootstrapped founders work hard, but on their own terms. No board meetings. No investor updates. No pressure to perform for others. That time adds up. I’ve talked to funded founders who spend 20% of their time on investor relations. That’s one full day per week not spent on the business.

Your decisions:

Every choice is yours. Take the business where you want. Serve clients you like. Build culture that matters to you. Turn down work that doesn’t fit.

Your future:

No exit pressure. No timeline constraints. The business serves you, not the other way around.

This freedom has economic value. It’s just not the kind VCs measure.

The Bottom Line

Venture capital exists for businesses with specific characteristics: near-zero marginal costs, network effects, winner-take-all markets, potential for 100x returns.

Service businesses have different characteristics: linear scaling, relationship dependency, margin constraints, moderate exit multiples.

Forcing the VC model onto service businesses works poorly for everyone. Founders lose control and often wealth. Investors get disappointing returns. Employees face instability.

Bootstrapping aligns incentives. It preserves optionality. It creates sustainable wealth over time rather than lottery-ticket outcomes.

The case against venture capital for service businesses isn’t philosophical. It’s practical. For more on building sustainable freelance and agency businesses, see our guides on must-have tools for freelancers and WordPress freelancing.

The model doesn’t fit. Don’t force it.

Venture Capital FAQ

Frequently Asked Questions

Why don’t service businesses fit the venture capital model?

Service businesses scale linearly: more revenue requires more people, which adds management overhead proportionally. VCs need 10-100x returns, but service businesses typically exit at 1-3x revenue versus 10x+ for software companies. Margins often compress with growth as senior talent demands higher salaries. Client relationships depend on specific people, making exits difficult. The fundamental economics just don’t support venture-scale returns.

What problems does taking VC money create for agencies?

Growth pressure forces rapid hiring, which causes quality dilution and culture erosion. VCs push to sacrifice profitability for growth, creating cash flow crises. Founder ownership dilutes across funding rounds to 20-30%. Exit pressure forces decisions that serve investors, not the business. And the timeline mismatch is real: VCs need exits within 8-10 years, while service businesses thrive when built for decades. I’ve watched agencies go through this cycle three times in five years.

What advantages do bootstrapped service businesses have?

Day-one revenue from selling time and expertise. Low capital requirements, just a laptop and skills. Immediate profitability when properly priced. Complete control over decisions, direction, and timeline. No board meetings or investor updates. Optionality to continue, sell, or wind down on your own terms. My first month freelancing, I billed $3,200. No VC check required. After sixteen years, that freedom is worth more than any investment offer.

How much can a bootstrapped agency actually earn?

Bootstrapped agencies can reach $10M, $50M, even $100M+ in revenue with substantial founder ownership. A $5M agency generating 20% profit throws off $1M annually. Maintain that for a decade and you’ve extracted $10M while building equity worth $5-15M. No VC would fund this outcome, but it creates life-changing wealth. And you own 100% of it without liquidation preferences or dilution eating into your returns.

When might funding actually make sense for a service business?

Three edge cases: when you’re building software that automates service delivery (transitioning to a software company), when pursuing market consolidation through acquiring competitors (financial engineering, different risks), or when building a true platform matching service providers with clients (technology business wrapped in services). For most traditional service businesses, these exceptions don’t apply. The default should be bootstrapping.

How does a bootstrapped service business fund its growth?

Revenue grows first, then expenses. Never reverse that order. Price for profit from day one so every project generates margin. Hire only when funded by existing recurring revenue, not projected revenue. Reinvest retained earnings for organic growth. Build recurring revenue through retainers and maintenance contracts. The constraint of self-funding forces discipline about which investments actually matter. When it’s your money, you think harder about where it goes.

What happens when funded competitors enter my market?

Funded competitors often look scary but frequently implode. Aggressive hiring creates management chaos. Marketing spend rarely works for trust-based services. Price undercutting destroys their margins without capturing loyal clients. I’ve outlasted several funded competitors over sixteen years. The bootstrapped businesses survive recessions and market shifts because they’re built for resilience. The funded ones are built for explosive growth, and when growth stalls, they collapse.

Is bootstrapping a service business harder than raising funds?

Bootstrapping is slower but significantly less risky. You grow at the pace your revenue supports rather than at the pace investors demand. The difficulty is different: bootstrapping requires patience and financial discipline, while VC-funded growth requires managing investor expectations, rapid team scaling, and exit pressure. Most founders I know who bootstrapped successfully say they’d never trade their freedom for funding. The math often favors bootstrapping in total wealth and quality of life.